We retain "BUY" rating with a Target Price of Rs. 505 (vs Rs 525 earlier). Rashi Peripherals ltd reported decent topline growth, on the back of strong sales from the PES segment (PCs, Desktops). Our dealer checks suggest demand is improving for AI-enabled PCs as prices are more attractive on a YoY basis. Ecommerce contributed 17% of sales in Q2 (seasonally strong quarter), which added pressure on margins along with ESOP expenses. Cashflow turned positive on the back of better working capital management; management is confident of turning OCF positive for FY26e and beyond. We believe the pick-up in the replacement cycle for PC’s in H2FY26 coupled with improved demand for data center products will be a positive catalyst for Rashi over the next 2-years.

The company reported revenue growth of 31.8% QoQ / 12.1% YoY, primarily due to strong demand for PCs in the consumer segment. Industry grew at 5-6%, while Rashi continued to grow 2x of industry growth. ICT sector is expected to grow 8-10% in H2, which bodes well for Rashi. Within the PES segment, AI-PCs have started to gain traction especially on the enterprise side. The co. is looking to participate in large deals from H2FY26, which bodes well for growth. The deal with Dell could potentially add Rs10bn of revenue annually.

EBITDA margins came in at a 2.5% on account of higher contribution of online sales and ESOP expenses. Lower employee costs and other expenses helped the co. to sustain margins above 2.5%. We expect the margins to normalize to 2.7-3% over the next few quarters as the company focuses on growth. The company did not clock any large deals in Q2 which helped margins. Additionally, the company increased its brand portfolio from 74 to 79 in Q1, adding global and Indian brands.

The strategic change from chasing larger enterprise deals (Yotta deal) to going after small and more frequent deals is reflected in better margins and predictable growth. The anticipated PC replacement cycle from H2FY26—driven by increased adoption of AI-enabled PCs—should aid growth. Cash generation improved in H1 on the back of better collection and working capital management backed by improved credit rating. We expect CFO to remain positive for FY26E, with ROCE to be in the range of 13-15%+. The exit of the Company Secretary and compliance officer is unlikely to impact business operations, as suitable replacements has already been appointed.

We are factoring in 12.2%/21.5%/14.9% CAGR in Revenue/EBITDA/PAT over FY25-28E. We value the company at 12x Sept’28E EPS, arriving at a TP of Rs505 (Rs 525 earlier) on the back of higher PES segment growth (lower margins vs LIT). Key risks: 1) Delay in replacement cycle for PC’s, 2) Supply related issues for components (CPUs, GPUs, RAM) 3) Failure to win large deals from data center projects.

Company website: https://rptechindia.com/

| Rating | BUY |

|---|---|

| CMP | INR 325 |

| Target Price | INR 505 |

| Upside | 55% |

Click to download the full Rashi Peripherals Limited Company Update

The company reported 31.8% QoQ and 12.1% YoY revenue growth, driven by strong demand in the PES segment, particularly PCs and desktops, outpacing overall industry growth of 5–6%.

Rashi turned cashflow positive due to better working capital management and improved collections. Management expects operating cash flow to remain positive in FY26 and beyond.

EBITDA margin stood at 2.5% in Q2, impacted by higher ecommerce contribution and ESOP expenses. Margins are expected to normalize to 2.7–3% over upcoming quarters.

Growth is expected from the PC replacement cycle, rising demand for AI-enabled PCs, expansion of the brand portfolio, and participation in large potential deals, including the opportunity with Dell.

The stock retains a BUY rating with a target price of ₹505, based on 12x Sept’28E EPS. The earlier target price was ₹525.

Key risks include delay in PC replacement cycle, supply chain issues for critical components such as CPUs and GPUs, and slower-than-expected wins in data center–related deals.

Disclaimer: - You are advised to read our disclaimer here: https://www.mnclgroup.com/disclaimers

Empower your finances with ReSach – the stock trading apptrusted by serious investors. Whether you're planning to invest in stocks, explore commodity trading, or need a financial advisor to guide you, Resach brings it all under one platform.

Start trading today with ReSach and unlock seamless investing on the go.

Name of the Company has changed from Networth Stock Broking Limited to Monarch Networth Capital Limited upon Certification of Incorporation received from Registrar of Companies, Mumbai vide certificate dated 13th October, 2015.

If you are not satisfied with the resolution provided, you can lodge your complaint online at: https://scores.sebi.gov.in/link

In case of grievance client can log on to the SMART ODR Portal, if they are unsatisfied with the response provided by us. Your attention is drawn to the SEBI circular no. SEBI/HO/OIAE/OIAE_IAD-1/P/CIR/2023/131 dated July 31, 2023, on “Online Resolution of Disputes in the Indian Securities Market”.

Purchase of REs only gives buyer the right to participate in the ongoing Rights Issue of the concerned company by making an application with requisite application money or renounce the REs before the issue closes. REs which are neither subscribed by making an application with requisite application money nor renounced, on or before the Issue closing date shall lapse and shall be extinguished after the Issue closing date. Please check your dp account for further details.

Please do not share your online trading password with anyone as this could weaken the security of your account and lead to unauthorized trades or losses.

Monarch Networth Capital Limited (‘MNCL’) | CIN No.: L64990GJ1993PLC120014

Unit No. 803-804A, 8th Floor, X-Change Plaza, Block No. 53, Zone 5, Road-5E, Gift City, Gandhinagar - 382050, Gujarat

Ahmedabad

“Monarch House”, Opp Prahladbhai Patel garden, Near Ishwar Bhuvan, Commerce Six Roads, Navrangpura, Ahmedabad - 380009

Mumbai

Monarch Networth Capital Limited, G Block, Laxmi Tower, B Wing, 4th Floor, Bandra Kurla Complex, Bandra East, Mumbai - 400051.

Email for Grievance: grievances@mnclgroup.com

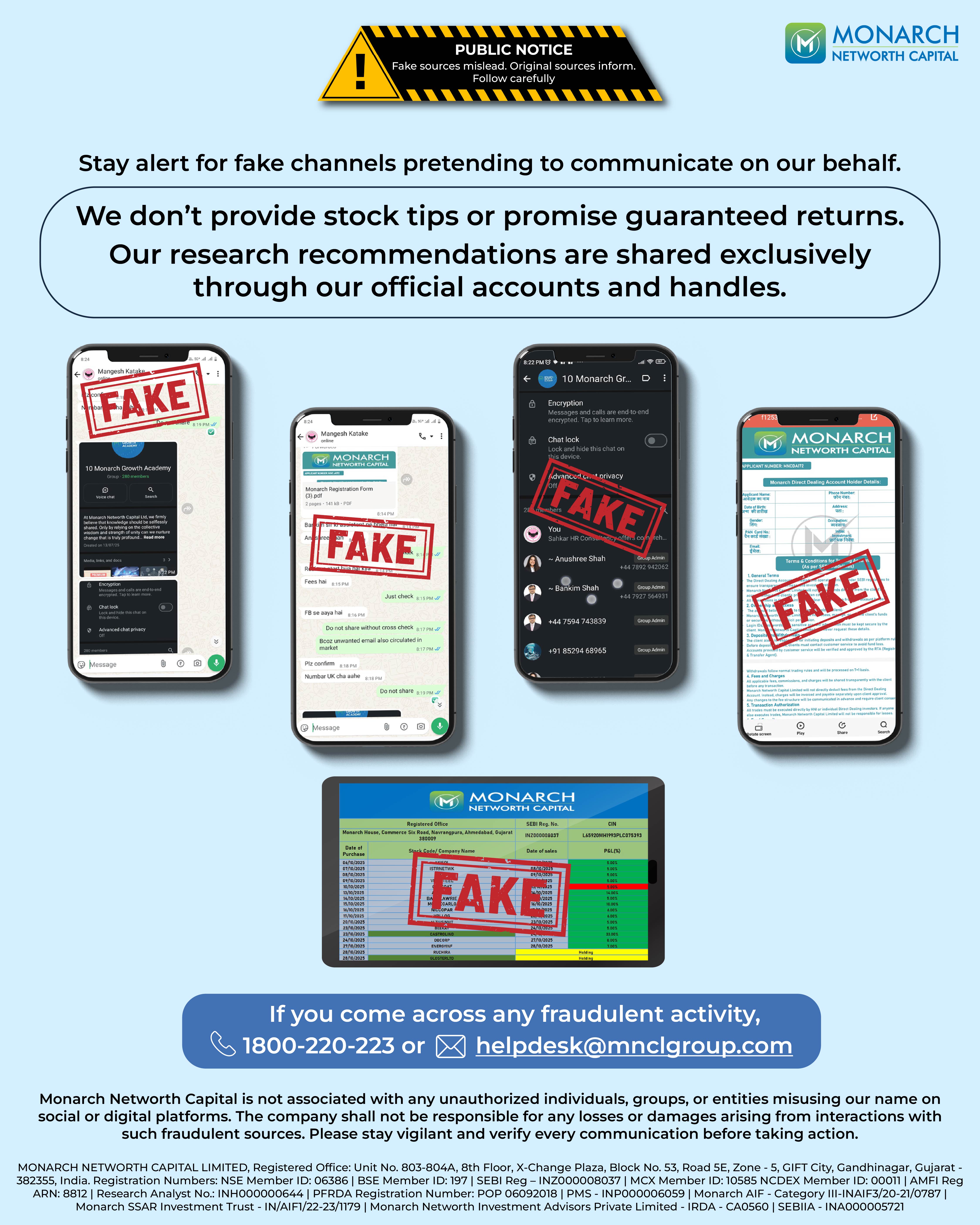

Investors are requested to note that Stock broker (Monarch Networth Capital Ltd) is permitted to receive money from investors through designated bank accounts only named as Up streaming Client Nodal Bank Account (USCNBA). Stock broker (Monarch Networth Capital Ltd) is also required to disclose these USCNB accounts to Stock Exchange. Hence, you are requested to use following USCNB accounts only (Click to View) for the purpose of dealings in your trading account with us. The details of these USCNB accounts are also displayed by Stock Exchanges on their website under “Know/ Locate your Stock Broker".

Mechanism for addressing grievances and information about SCORES.

Monarch Networth Capital IFSC Private Limited (Wholly owned subsidiary of Monarch Networth Capital Limited) is a Registered Fund Management Entity (Retail) having Registration No: IFSCA/FME/III/2025-26/169. Monarch India Growth Fund will be an open-ended Restricted Scheme (Non-Retail) construed as a Category III AIF under the IFSCA (Fund Management) Regulations, 2025. Monarch AIF is a Category III AIF having SEBI Registration No. IN/AIF3/20-21/0787. This material is for informational purposes only and is not intended as an offer or solicitation or investment advice to buy or sell securities. Investments are subject to market risks. The offering is made only through official scheme documents to eligible investors under GIFT IFSC regulations. Investors should read all documents carefully and consult their advisors before investing.

Mechanism for addressing grievances and information about SCORES.

Monarch Networth Capital Limited (‘MNCL’) | CIN No.: L64990GJ1993PLC120014

(As per LODR Regulations and Companies Act, 2013)

Contact information of the designated officials of the listed entity who are responsible for assisting and handling investor grievances : Mr. Nitesh Tanwar

Monarch Networth Capital Limited

Unit No. 803-804A, 8th Floor, X-Change Plaza, Block No. 53, Zone 5, Road-5E, Gift City, Gandhinagar - 382050, Gujarat

Ahmedabad

“Monarch House”, Opp Prahladbhai Patel garden, Near Ishwar Bhuvan, Commerce Six Roads, Navrangpura, Ahmedabad – 380009

Mumbai

Monarch Networth Capital Limited, G Block, Laxmi Tower, B Wing, 4th Floor, Bandra Kurla Complex, Bandra East, Mumbai - 400051.

Phone: 022 - 66476400 / 66476405

Email: cs@mnclgroup.com

Email for Grievance: cs@mnclgroup.com

Listing of Equity Shares on Stock Exchange at

BSE

NSE

(Formerly known as Link Intime India Private Limited)

For any queries related to broking please contact helpdesk@mnclgroup.com.

‘Investments in securities market are subject to market risks, read all the related documents carefully before investing.’