on a decisive journey into the world of retail broking services with Monarch Networth – your gateway to unmatched financial expertise and unwavering reliability.

on a decisive journey into the world of retail broking services with Monarch Networth – your gateway to unmatched financial expertise and unwavering reliability.For over three decades, Monarch Networth Capital Limited (MNCL) has been an unwavering force in the financial markets, solidifying its position as an indisputable pillar of trust. Our illustrious reputation resonates across the industry, symbolizing a commitment to value creation that has stood the test of time.

Operating in over 140+ cities, with 60 strategically located branches and a dynamic team of over 250 relationship managers, Monarch Networth ensures accessibility like no other. Our widespread presence underscores our dedication to bringing trustworthy financial solutions to your doorstep.

In an industry where data-driven decisions are paramount, Monarch Networth prioritizes conducting "Deep Research" on companies. This thorough analysis fosters strong conviction, which in turn drives value creation for our clients across all divisions, resulting in superior returns.

Monarch Networth’s commitment goes beyond numbers; it's about understanding and serving our clients. Our dedicated RMs ensure personalized financial solutions tailored to meet your unique needs and aspirations. Our client testimonials speak volumes about our conviction.

Achieving an impressive 80% strike rate on our investment calls, we combine rigorous research with a client-centric approach to consistently deliver exceptional value.

Monarch Networth stands out as a research-oriented and nimble financial services firm. It consistently surpasses...

As an investor, I have always looked for partners who can appreciate the nuances of...

Partnering with Monarch Networth has been a truly transformative experience. In the fast-paced world of...

Monarch Networth Capital has redefined my perception of financial services. As a recruitment consultant, I’m...

As a promoter focused on growing my business, I often find it challenging to dedicate...

I've been a part of Monarch Networth for the past four years, and my connection...

I have experienced a financial journey like never before with Monarch Networth. Investing with them...

The MNCL group takes pride in its prestigious accolades, notably honored as the "Best Regional Retail Broker" by NSE. This recognition not only validates our position as an industry leader but also showcases our unwavering commitment to excellence.

Monarch Networth isn't just a service provider; we are your partner in financial empowerment, offering a suite of retail broking solutions that elevate your financial journey to new heights. Join us in shaping a future where your financial aspirations become a reality!

Navigate the complexities of financial markets with our comprehensive derivatives trading services.

Dive into the world of equities with Monarch Networth, where every investment opens doors to new possibilities.

Seize opportunities in the commodities market Monarch Networth’s expert guidance and strategic insights.

Explore the dynamic world of currency trading, where Monarch Networth empowers you to make informed and profitable decisions.

Participate in Initial Public Offerings (IPOs) and access exciting new investment opportunities with Monarch Networth’s retail broking services.

Discover a world of tailored investment opportunities within our Retail Broking suite at Monarch Networth. From Derivatives and Equities Trading to Commodities and Currency Trading, each avenue is meticulously crafted to align with your unique investment preferences and objectives, ensuring a comprehensive and diverse trading experience.

Execute trades seamlessly through the web, mobile, or executable platforms, offering unparalleled flexibility tailored to your convenience.

Access an extensive reservoir of market research, empowering you to make astute trading decisions grounded in real-time, actionable data.

Enhance your investment journey with a dedicated relationship manager proficient in customizing strategies to align with your financial goals seamlessly.

Leverage derivatives as powerful tools to navigate market volatility strategically, ensuring a stable foundation for your investments.

Direct your investments towards burgeoning sectors, positioning yourself for sustained, long-term gains and staying ahead of emerging opportunities.

Achieve robust portfolio diversification through strategic commodity trading, effectively minimizing risk exposure and maximizing returns.

Rely on our round-the-clock back-office assistance, ensuring a constant lifeline of support whenever you require assistance – day or night. At Monarch Networth, your success is our priority, backed by a suite of features designed to elevate your trading experience to new heights.

At Monarch Networth Capital Limited, we embrace a client-centric commitment deeply grounded in a nuanced understanding of diverse business models, showcasing our unwavering dedication to ensuring your utmost satisfaction. Our fundamental strength lies in the precise execution of high-quality strategies, assuring that your investments yield optimal and desired outcomes.

We vehemently discourage the practice of churn, recognizing that it invariably leads to retail investors losing their hard-earned money. Our core principle is straightforward: our success is intertwined with the prosperity of our clients.

Our responsibility is to demystify the complexities of the investment landscape. We are committed to providing practical advice, enabling you to attain your financial objectives with unparalleled clarity and honesty.

Our client-centric approach goes beyond conventional norms. We take pride in crafting personalized solutions tailored to your unique financial goals, ensuring a partnership that extends beyond transactions to foster enduring success.

Understanding that every investment carries inherent risks, we proactively implement robust risk mitigation strategies. This ensures that your portfolio is resilient in the face of market fluctuations, safeguarding your financial interests.

The financial landscape evolves, and so do we. Our commitment to continuous learning and adaptation means that you benefit from strategies informed by the latest market trends and innovations.

We believe in empowering our clients through knowledge. Our educational initiatives provide you with the tools and insights needed to make informed decisions, promoting financial literacy and empowerment.

Open and transparent communication is at the heart of our client relationships. We ensure accessibility, responsiveness, and clear communication channels to keep you informed and confident in your investment journey.

We view our relationship with clients as a strategic partnership. Your success is our success, and we actively seek opportunities to align our strategies with your evolving financial aspirations.

Unit No. 803-804A, 8th Floor,

X-Change Plaza, Block No. 53,

Zone 5, Road-5E, Gift City,

Gandhinagar - 382050, Gujarat

Email : reachus@mnclgroup.com

Monarch House,

Opp. Prahladbhai Patel Garden,

Near Ishwar Bhuvan,

Commerce Six Road, Navrangpura,

Ahmedabad-380009

Monarch Networth Capital

Limited, G Block,

Laxmi Tower, B Wing,

4th Floor, Bandra Kurla Complex,

Bandra East, Mumbai – 400051.

Connect with Monarch Networth Capital Limited

For inquiries or assistance related to our financial services, feel free to reach out to our dedicated team.

We are committed to providing prompt and reliable support. You can write to us at

fund@monarchifsc.com

Your financial success is our priority, and we look forward to assisting you in your journey.

Commodities are tangible goods, such as food grains, industrial crops, bullion, metals, and crude oil, often used in large quantities for production or direct consumption. Their uniformity, like one unit of gold being indistinguishable from another, makes them suitable for trading.

Commodity derivatives encompass a wide range of agricultural and mined products, such as crude oil, natural gas, gold, silver, copper and aluminum, offering diverse trading opportunities.

Derivatives are financial instruments deriving their value from underlying assets, such as equities, currencies, or commodities. For example, futures contract prices of Reliance Industries (RIL) are tied to the performance of RIL's shares.

Commodity derivatives markets provide a nationwide platform for price discovery and risk hedging, fostering organized and trustworthy trading environments. They offer unbiased price signals, aiding production planning and trading decisions.

Commodity derivatives trading involves standardized contracts of agricultural and non-agricultural commodities traded electronically on recognized commodity exchanges or select stock exchanges, subject to regulatory approvals.

Currency trading involves the simultaneous purchase and sale of one currency against another, such as USD versus INR, providing opportunities for trading and hedging.

Exchange Traded Currency Futures and Options are standardized contracts traded on exchanges featuring fixed contract sizes and expiry dates.

A trading account is an account that allows both investors and traders to buy and sell various financial assets like stocks, bonds, commodities, currencies or other securities.

A demat account is like a bank account that facilitates the digital transfer of shares and securities, replacing the need for physical certificates. It enhances security and reduces the risks associated with physical security.

Equity investments historically offer superior long-term returns compared to other financial assets, such as fixed deposits, government savings schemes, real estate, or commodities. Indian equities have displayed impressive CAGR returns of 15-16% over the past decade, underlining their immense potential.

To open a demat and trading account, you need Aadhar and PAN cards, income proof, a webcam for personal identification, and a cancelled cheque. Our E-KYC linked account opening process is designed for simplicity and efficiency, requiring just a few steps.

Knowing when to buy and sell stocks, involves analyzing several factors, including market conditions, company performance, and broader economic indicators. Analysis can be done based on Fundamentals & Technical indicators. The fundamental analysis involves evaluating a company's financial health and overall potential for growth while technical analysis relies on charts and patterns to predict future price movements.

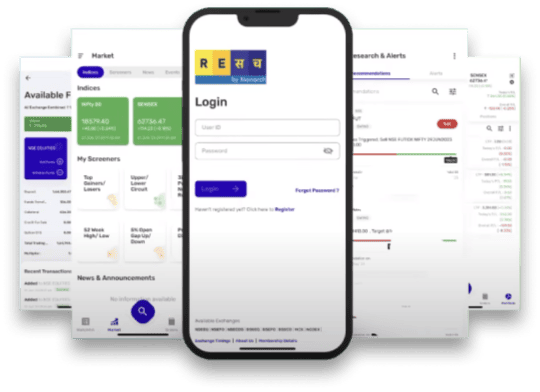

We prioritize personalized service and assign dedicated relationship managers to each client. These managers handle order execution; provides account/ portfolio updates and offer valuable investment and trading advice. Additionally, our user-friendly ReSACH mobile app provides seamless experience for online trading and investing

Certainly, you have the option to place an order via a phone call. We operate through secure lines, recording all transactions to guarantee the authenticity of your trades.

Our mobile app allows you to buy and sell shares with ease. You can monitor your portfolio, track returns, and manage mutual fund holdings conveniently. It's a comprehensive platform for on-the-go trading.

Derivative instruments can be broadly categorized into two types: Futures and Options. Futures involve an agreement to buy or sell an asset at an agreed price and time, while Options provide the right, but not the obligation, to buy or sell an asset at a specific price and time.

To invest in derivatives, you can open a trading account with a SEBI-registered broker like Monarch and activate the relevant derivative segment(s) (e.g., Equities, Commodities, or Currencies). This enables you to participate in derivatives trading.

Derivatives offer inherent leverage, potentially enhancing returns when used with discipline. They also provide valuable tools for portfolio risk management through various strategies.

Derivatives are leveraged instruments, and while they can be valuable, they require careful risk management. When used judiciously and with a sound strategy, they can be a powerful asset for generating returns and managing portfolio risk.

In addition to KYC documents for opening a trading account, you'll need to provide one of the following: a six-month bank statement, the latest ITR Acknowledgement copy, Form 16 for salary income, the latest salary slip, the latest DMAT holding statement, or a net worth certificate certified by a chartered accountant to activate the F&O segment.

Choosing stocks for investment involves careful research into a company's financial health, competitive position, industry trends, and growth potential. Assess factors like earnings, cash flow generation, management quality, and long-term sustainability to make informed decisions.

Intraday trading requires a focus on short-term price movements. Look for stocks with high liquidity, volatility and technical analysis indicators like moving averages and RSI to identify potential intraday opportunities.

For short-term investments, focus on stocks with catalysts like earnings reports or news events. Utilize technical analysis to pinpoint entry and exit points while managing risk through stop-loss orders.

Long-term stock selection emphasizes stability, growth potential, and a buy-and-hold strategy. Prioritize companies with strong fundamentals, competitive advantages, and a history of consistent performance.

Derivatives can amplify returns but require skills and risk management. Develop a solid trading plan, use technical and fundamental analysis, and set clear entry and exit strategies to profit from derivatives.

Online trading in the Indian stock market involves opening a Trading & Demat account, placing orders, and monitoring your positions through a secure online platform. Our experts can guide you through this digital onboarding process.

Online trading encompasses various forms, including equity trading, commodity trading, currency trading, and derivatives trading. Each type has its own risk-reward profile, catering to different investment and trading strategies.

The equity trade life cycle encompasses a structured series of steps, commencing with order placement, where investors specify their desired stock transactions, and concluding with trade settlement, where cash and securities are exchanged.

Empower your finances with ReSach – the stock trading apptrusted by serious investors. Whether you're planning to invest in stocks, explore commodity trading, or need a financial advisor to guide you, Resach brings it all under one platform.

Start trading today with ReSach and unlock seamless investing on the go.

"Given a 10% chance of a 100 times payoff, you should take that bet every time."

Jeff Bezos

Name of the Company has changed from Networth Stock Broking Limited to Monarch Networth Capital Limited upon Certification of Incorporation received from Registrar of Companies, Mumbai vide certificate dated 13th October, 2015.

If you are not satisfied with the resolution provided, you can lodge your complaint online at: https://scores.sebi.gov.in/link

In case of grievance client can log on to the SMART ODR Portal, if they are unsatisfied with the response provided by us. Your attention is drawn to the SEBI circular no. SEBI/HO/OIAE/OIAE_IAD-1/P/CIR/2023/131 dated July 31, 2023, on “Online Resolution of Disputes in the Indian Securities Market”.

Purchase of REs only gives buyer the right to participate in the ongoing Rights Issue of the concerned company by making an application with requisite application money or renounce the REs before the issue closes. REs which are neither subscribed by making an application with requisite application money nor renounced, on or before the Issue closing date shall lapse and shall be extinguished after the Issue closing date. Please check your dp account for further details.

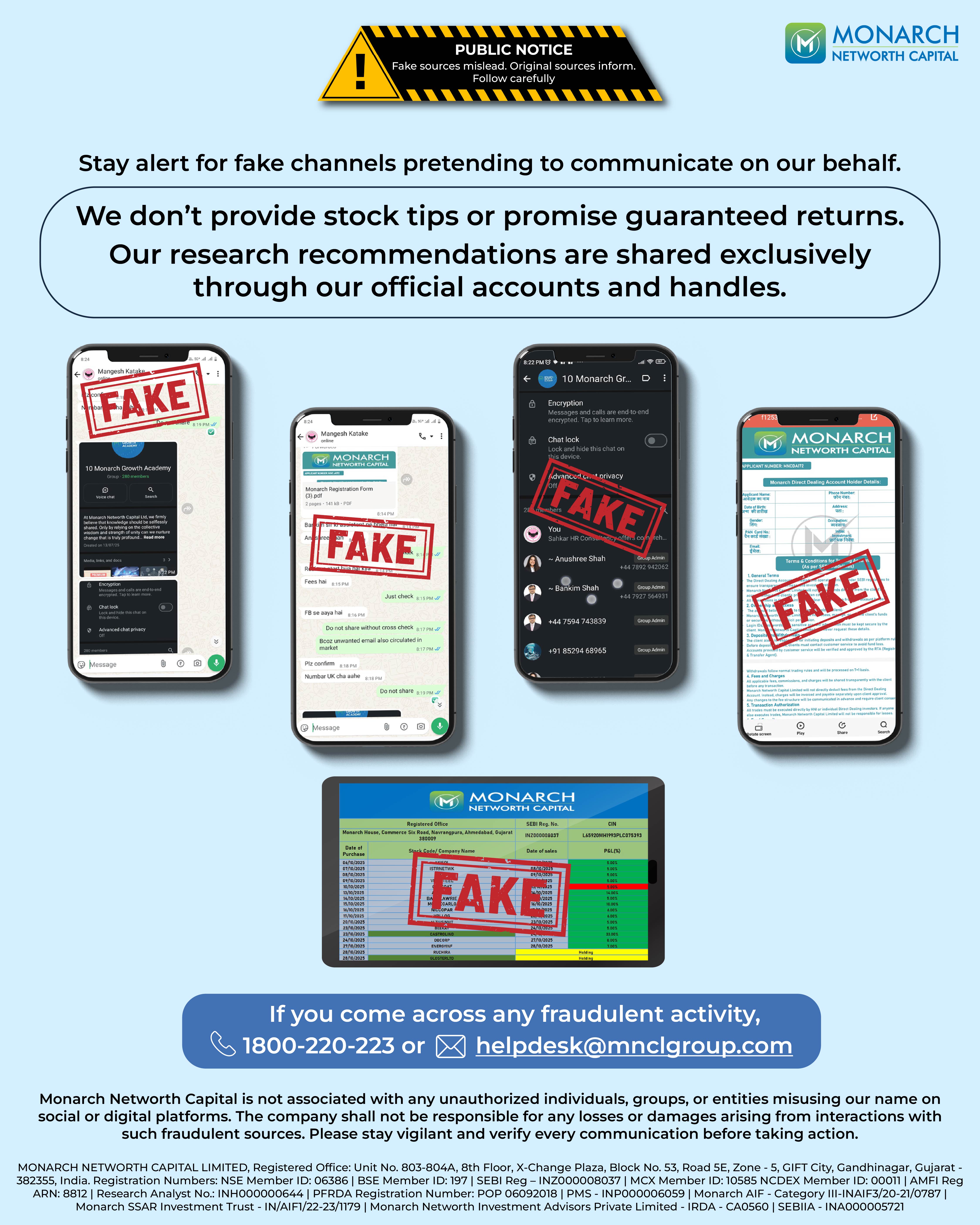

Please do not share your online trading password with anyone as this could weaken the security of your account and lead to unauthorized trades or losses.

Monarch Networth Capital Limited (‘MNCL’) | CIN No.: L64990GJ1993PLC120014

Unit No. 803-804A, 8th Floor, X-Change Plaza, Block No. 53, Zone 5, Road-5E, Gift City, Gandhinagar - 382050, Gujarat

Ahmedabad

“Monarch House”, Opp Prahladbhai Patel garden, Near Ishwar Bhuvan, Commerce Six Roads, Navrangpura, Ahmedabad - 380009

Mumbai

Monarch Networth Capital Limited, G Block, Laxmi Tower, B Wing, 4th Floor, Bandra Kurla Complex, Bandra East, Mumbai - 400051.

Email for Grievance: grievances@mnclgroup.com

Investors are requested to note that Stock broker (Monarch Networth Capital Ltd) is permitted to receive money from investors through designated bank accounts only named as Up streaming Client Nodal Bank Account (USCNBA). Stock broker (Monarch Networth Capital Ltd) is also required to disclose these USCNB accounts to Stock Exchange. Hence, you are requested to use following USCNB accounts only (Click to View) for the purpose of dealings in your trading account with us. The details of these USCNB accounts are also displayed by Stock Exchanges on their website under “Know/ Locate your Stock Broker".

Mechanism for addressing grievances and information about SCORES.

Monarch Networth Capital IFSC Private Limited (Wholly owned subsidiary of Monarch Networth Capital Limited) is a Registered Fund Management Entity (Retail) having Registration No: IFSCA/FME/III/2025-26/169. Monarch India Growth Fund will be an open-ended Restricted Scheme (Non-Retail) construed as a Category III AIF under the IFSCA (Fund Management) Regulations, 2025. Monarch AIF is a Category III AIF having SEBI Registration No. IN/AIF3/20-21/0787. This material is for informational purposes only and is not intended as an offer or solicitation or investment advice to buy or sell securities. Investments are subject to market risks. The offering is made only through official scheme documents to eligible investors under GIFT IFSC regulations. Investors should read all documents carefully and consult their advisors before investing.

Mechanism for addressing grievances and information about SCORES.

Monarch Networth Capital Limited (‘MNCL’) | CIN No.: L64990GJ1993PLC120014

(As per LODR Regulations and Companies Act, 2013)

Contact information of the designated officials of the listed entity who are responsible for assisting and handling investor grievances : Mr. Nitesh Tanwar

Monarch Networth Capital Limited

Unit No. 803-804A, 8th Floor, X-Change Plaza, Block No. 53, Zone 5, Road-5E, Gift City, Gandhinagar - 382050, Gujarat

Ahmedabad

“Monarch House”, Opp Prahladbhai Patel garden, Near Ishwar Bhuvan, Commerce Six Roads, Navrangpura, Ahmedabad – 380009

Mumbai

Monarch Networth Capital Limited, G Block, Laxmi Tower, B Wing, 4th Floor, Bandra Kurla Complex, Bandra East, Mumbai - 400051.

Phone: 022 - 66476400 / 66476405

Email: cs@mnclgroup.com

Email for Grievance: cs@mnclgroup.com

Listing of Equity Shares on Stock Exchange at

BSE

NSE

(Formerly known as Link Intime India Private Limited)

For any queries related to broking please contact helpdesk@mnclgroup.com.

‘Investments in securities market are subject to market risks, read all the related documents carefully before investing.’